Jan 27, 2016 | Uncategorized

We recently decided to get involved with a project that intrigued an employee here at The Law Office of David R Rocheford Jr.

We recently decided to get involved with a project that intrigued an employee here at The Law Office of David R Rocheford Jr.

Amber brought Right-To-Write information to Attorney Rocheford and he immediately saw the need and understood the mission. Their story is very inspiring and we felt it a good fit for our group, thank you Amber!

Please take a look…

In many parts of the world, owning a pen or pencil is a luxury that some families cannot afford. It is hard to imagine. Receiving an education without a writing utensil is even harder to imagine. Education can help achieve success and stability in a person’s life but without the basics, it is so much harder.

afford. It is hard to imagine. Receiving an education without a writing utensil is even harder to imagine. Education can help achieve success and stability in a person’s life but without the basics, it is so much harder.

Right-to-Write is a unique and simple program designed to put new and used pens and pencils to good use by collecting and then dispensing them to children in developing countries. Donated pens and pencils are delivered to schools, orphanages, and hospitals by individual volunteers, travelers, and organizations who can distribute them hand to hand, person to person, to children who need them. Through this effort Right-to-Write achieves many unique positive goals:

- facilitating better education for kids

- recycle pens and pencils that are “extras” in offices, handbags, houses, etc.

- promoting positive global alliances and friendships through direct face-to-face contact

- ensuring delivery and avoiding delivery cost, blackmarkets, and lost goods

Please check out their website to learn more. Simply drop your pens and pencils at our collection bin in our office lobby, preferably in a ziploc bag.

Jan 12, 2016 | Uncategorized

Leominster, MA January 8, 2016 – Real estate transactions are complicated and it is important for people to fully understand the process before making a decision to put their home on the market. In an effort to make the process easier for sellers, Attorney David Rocheford Jr. is proud to announce the release of his new book, “Selling Your Home in Massachusetts: How to sell on time, reduce your risk, and move on to your next property.” Rocheford has a real estate law practice and is dedicated to helping people sell their homes successfully. Guidelines vary by state, so the book covers everything sellers in Massachusetts need to know in order to understand the law and how to sell properly. It will be released on December 15, 2015 and it will be available on Amazon.com, and on the Rocheford’s website www.TheBestClosings.com.

Leominster, MA January 8, 2016 – Real estate transactions are complicated and it is important for people to fully understand the process before making a decision to put their home on the market. In an effort to make the process easier for sellers, Attorney David Rocheford Jr. is proud to announce the release of his new book, “Selling Your Home in Massachusetts: How to sell on time, reduce your risk, and move on to your next property.” Rocheford has a real estate law practice and is dedicated to helping people sell their homes successfully. Guidelines vary by state, so the book covers everything sellers in Massachusetts need to know in order to understand the law and how to sell properly. It will be released on December 15, 2015 and it will be available on Amazon.com, and on the Rocheford’s website www.TheBestClosings.com.

The book was written for people who are thinking about putting their house on the market, or, who are in the process of selling their home. It covers a wide variety of topics important to selling a home including the role of a real estate attorney, written agreements, the difference between real estate agents and Realtors®, property marketing, house pricing, commissions, fees and more. Rocheford takes complicated topics and simplifies them in a way that readers can understand and benefit from. According to Rocheford, “I educate the reader about how to get started and navigate the process of selling a home. This new book is an easy-to-follow, guide that was not written in typical ‘legalese’ that only attorneys understand. Everyone should fully understand the process before closing.”

Rocheford has over 20 years of experience in real estate. As a college student, Rocheford worked as a real estate agent and continued the job throughout law school. He opened his own law firm and focuses on real estate matters. With over 7,000 real estate transactions under his guidance, Rocheford knows what tips to give sellers and what mistakes to avoid. He is dedicated to simplifying the home selling process with his experience and knowledge in the field.

Nov 24, 2015 | Uncategorized

Make sure all of your clients are protected

You’re a real estate agent, so you know that buying a home can be overwhelming for many of your clients. Homebuyers can easily feel confused and frustrated by the mounds of paperwork they have to sign. Plus, all the fees associated with closing can sometimes be a surprise even to an experienced buyer.

You’re a real estate agent, so you know that buying a home can be overwhelming for many of your clients. Homebuyers can easily feel confused and frustrated by the mounds of paperwork they have to sign. Plus, all the fees associated with closing can sometimes be a surprise even to an experienced buyer.

Owner’s title insurance is one of those items often misunderstood by homebuyers at closing, yet its value is tremendous. As an important advisor to your clients, you are in the position to help them understand the value of owner’s title insurance and the dangers that can be incurred without it.

What is title insurance?

Owner’s title insurance is a policy that protects homebuyers’ property rights. For the same reasons that the bank requires a lender’s insurance policy, a homebuyer obtains owner’s title insurance to protect their legal claims to the property.

How it protects your clients

Say, for example, your client recently purchased a new home from a builder, but the builder failed to pay the roofer. Wanting to be paid, the roofer filed a lien against the property. Without owner’s title insurance, your client would be responsible for paying this existing debt—meaning they’d be paying the roofer out of pocket instead of purchasing something nice for their new home, like new living room furniture. This is just one example of how owner’s title insurance protects homebuyers’ from various significant risks. With owner’s title insurance, your client would be protected from certain legal or financial responsibilities.

Enduring value

The good news is that owner’s title insurance protects homebuyers financially, as long as they or their heirs* own the home. For a low, one-time fee (average of 0.5% of purchase price), homebuyers can rest assured, knowing they are protected from inheriting existing debts or claims to their property.

State regulations and CFPB

Each state government regulates its own title insurance costs. In addition, the Consumer Financial Protection Bureau (CFPB) regulates closing and settlement practices which can impact title insurance. Keep in mind that title insurance industry practices vary due to differences in state laws and local real estate customs. The party that pays for the owner’s title insurance policy varies from state to state, and sometimes even within a state. For more information about title insurance, or to find a company approved to issue an owner’s policy, please direct your homebuyer clients to www.homeclosing101.org.

Free resources for Realtors®

Together, real estate agents, land title insurance professionals and other stakeholders involved in real estate transactions can protect homebuyers and provide them with the peace of mind they deserve during the home closing process.

For more information about title insurance, and to get free resources for real estate agents, visit www.alta.org/realtor.

Sep 14, 2015 | Uncategorized

You may have seen this statement in the remarks section of property descriptions and  purchase and sale agreement: “This property is being sold subject to 24 CFR 206.125”. REO sellers are required by HUD to comply with this regulation upon the acquisition and resale of the property. The regulation pertains to properties that were subject to a reverse mortgage. Reverse mortgages are sometimes known as Home Equity Conversion Mortgages (HECM). Reverse mortgages are available to qualified borrowers over 62 years of age often the properties were transferred back to the lender due the death of the owner rather than as a result of a financial or fraudulent situation. It is likely that property is currently an REO because of the drop in in the value of homes since the peak of the market when some lenders were aggressively marketing reverse mortgages. The expectation at that time was that values would continue to increase. These REOs typically don’t have any owner occupant or NSP buyer restrictions when they come on the market. There are a couple of things to note with them. They generally will not sell the property for less than the asking price which is usually an as-is appraised value established by an FHA roster Appraiser. They are sold As-Is at the time of closing with no repair reimbursements or allowances. They won’t pay for home warranties. Home inspections and the connections of utilities for inspections will be at the buyer’s expense. Also the seller will not contribute to buyer’s closing costs. They should be viewed as soon as they come on the market because some of them are very good values and end up having multiple offers on them.

purchase and sale agreement: “This property is being sold subject to 24 CFR 206.125”. REO sellers are required by HUD to comply with this regulation upon the acquisition and resale of the property. The regulation pertains to properties that were subject to a reverse mortgage. Reverse mortgages are sometimes known as Home Equity Conversion Mortgages (HECM). Reverse mortgages are available to qualified borrowers over 62 years of age often the properties were transferred back to the lender due the death of the owner rather than as a result of a financial or fraudulent situation. It is likely that property is currently an REO because of the drop in in the value of homes since the peak of the market when some lenders were aggressively marketing reverse mortgages. The expectation at that time was that values would continue to increase. These REOs typically don’t have any owner occupant or NSP buyer restrictions when they come on the market. There are a couple of things to note with them. They generally will not sell the property for less than the asking price which is usually an as-is appraised value established by an FHA roster Appraiser. They are sold As-Is at the time of closing with no repair reimbursements or allowances. They won’t pay for home warranties. Home inspections and the connections of utilities for inspections will be at the buyer’s expense. Also the seller will not contribute to buyer’s closing costs. They should be viewed as soon as they come on the market because some of them are very good values and end up having multiple offers on them.

Mar 4, 2015 | Uncategorized

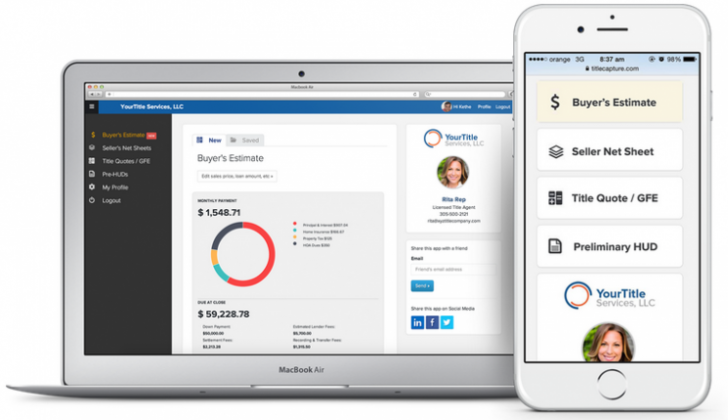

Realtors®, Mortgage Lenders, Loan Officers and Agents register for access to our fee quote service.

Get instant title quotes, settlement fees, borrower estimates, and Pre-HUDs. Store your client quotes, net sheets and HUDs in your secure, private account. Once saved you can print or email them to your clients directly from your account. You will have convenient, easy, online access to your stored quotes and office contact information from your mobile device and desktop 24/7.

- Instant title quotes, seller’s net sheets, and Pre-HUDs

- Store your quotes, net sheets, and HUDs

- Send them to your clients via email

- Easy access to your title attorney’s contact details

- Mobile & Desktop online access 24/7

Contact David for more information: 978-728-5104

Oct 22, 2014 | Uncategorized

By Amy Tierce

Good salespeople are always trying to improve their game, to up the ante and grow. Many salespeople get sucked into the ‘shiny-new-object’ trap. They’re looking for the next big thing to implement: a strategy, an app, a new program or campaign. They ask themselves, “What’s the next breakthrough product that will take my career to a higher level?”

I’m in the process of building a whole new business and all day long I’m engaged in networking with salespeople, referral partners and business leaders as we grow our presence in New England. As I was struggling to lay out a business plan, I finally asked myself an important question “You’ve done this before. What worked then, will it work today, and why aren’t you doing it?” At that moment, I realized that I didn’t need to create a new strategy – I needed to review my past success and replicate the actions that got me there. Perhaps I could add a tweak or two for the times, but don’t mess with what’s worked.

I counsel you to ask yourself those same questions.

We’re frequently chasing the next new thing when we already have all the tools, ideas and action plans necessary to achieve our present goals. Much like Dorothy in The Wizard of Oz – the power was always there, but her thoughts prevented her from seeing it.

Try to recall the best professional week – or month, or quarter, or year, or any period of time – that you’ve experienced in your career. What were you doing? What was working for you? Where did the energy come from? What made that period feel good? What made that a successful time for you?

Figure that out – then do it again, and repeat!

Instead of looking for the next big thing, dig deep and look at what actions have been a big thing in your career. Then consider how to recreate them, or continue doing them with greater consistency!

.

Amy Tierce is Regional is Vice President at Winturst Mortgage

She can be reached at: (781) 453-8900

atierce@wintrustmortgage.com

www.TheTierceTeam.com